Proactive Retirement Strategies Using The SECURE Act

- 15

- Mar

In February of 2022, the IRS and Department of Treasury released 275 pages of proposed regulations to implement the SECURE Act (Setting Every Community Up for Retirement Enhancement), that was originally enacted in December 2019. The SECURE Act was designed to increase access to retirement plans and encourage retirement saving for many Americans. It also changed the rules for retirement plan withdrawals after the original owner’s death. The proposed regulations clarify some of the outstanding technical questions on rules and definitions, including:

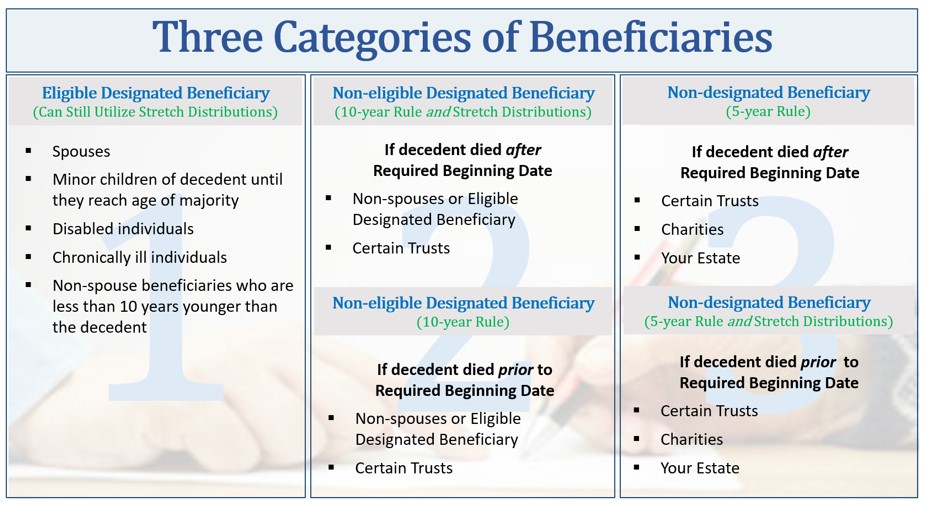

- The definition of Eligible Designated Beneficiaries;

- The Required Minimum Distributions (RMD) startin gage for surviviing spouse beneficiaries;

- New operating rules for retirement accounts payable to trusts;

- New rules which specifically allow greater latitude to design and administer IRA trusts without violating the “identifiable beneficiary” see-through trust retirements; and

- Providing Non-eligible Designated Beneficiaries are subject to both annual RMDs and the 10-year rule.

One of our goals as your financial professional is to keep you aware of any updates to fiduciary or tax laws that we feel may affect your unique situation. Please remember, the SECURE ACT is a very complex area of tax code. Those who are affected by it should always seek the guidance of a financial and/or tax professional.

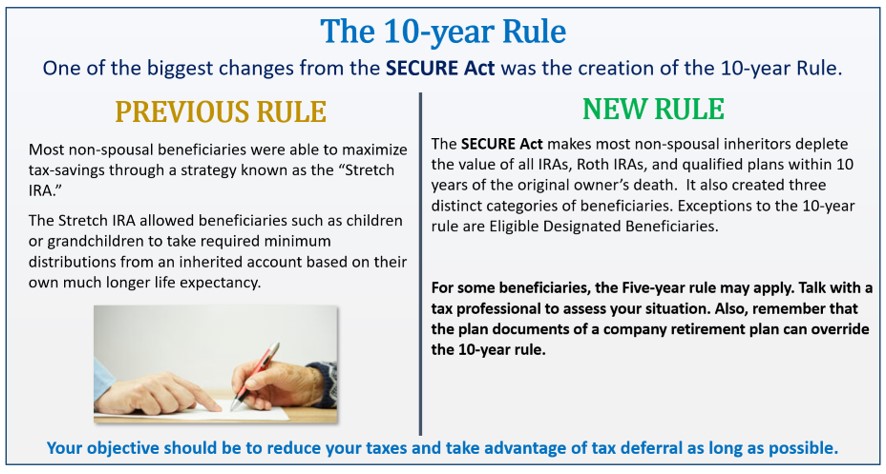

The Elimination of “Stretch” IRAs & The 10-Year Rule

The “Stretch IRA” for all has been eliminated. The SECURE Act made the Stretch IRA only available to Eligible Designated Beneficiaries. If the original owner of an IRA passes away after December 31, 2019, fewer beneficiaries will be able to extend distributions from the inherited IRA over their lifetime. Many will instead need to withdraw all assets from the inherited IRA within 10 years following the death of the original account holder.

The proposed regulations clarify post-mortem distribution requirements. A “Non-eligible, qualified Designated Beneficiary “ is subject to the 10-year rule. If death occurred prior to the Required Beginning Date (RBD; age 72), no annual RMDs are requires; the account merely must be fully distributed by year-10. However, if death occurred after the RBD, the beneficiary must take distributions based on their life expectancy and the entire account must be fully distributed by year-10.

Please note that this rule applies to deaths that occur after December 31, 2019. Anyone who inherited an IRA before 2020 is generally grandfathered in under the old rules. The major exception is that if a beneficiary dies before the entire inherited IRA is distributed, the 10-year rule now applies. (Under the old rules distribution continued according to the deceased’s beneficiary’s schedule.)

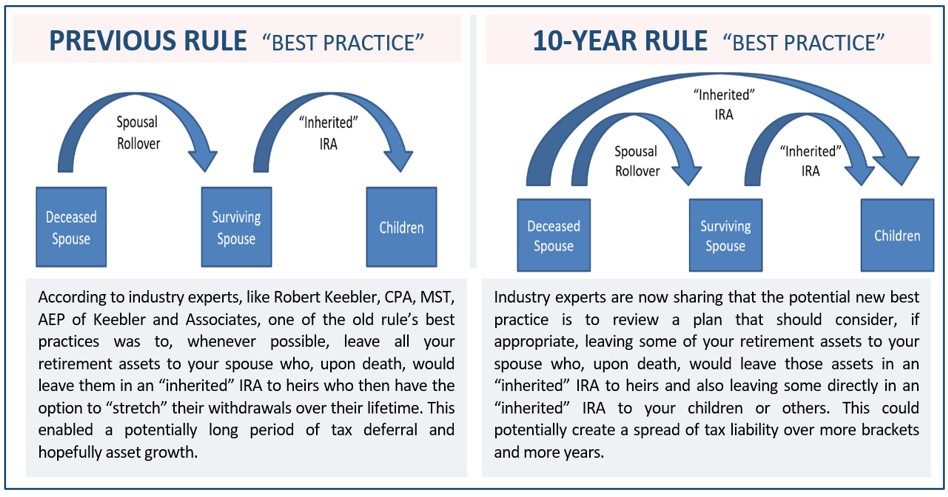

This 10–Year rule reminds us that a proactive planning approach could reap rewards. To maximize your situation under the new 10-year rule, you may want to consider Roth IRA conversions and possibly spreading distributions over many years and lower tax brackets. Unlike distributions from regular IRAs, Roth IRA qualified distributions are not taxed. There are potential benefits to converting to a Roth IRA, including:

- Lowering overall taxable income long-term.

- Enjoying tax-free compounding.

- Have no RMDs at age 72.

- Allows tax-free withdrawals for beneficiaries.

There are limitations to who and how you can convert to a Roth IRA. Making any changes to your retirement plan could have tax and other implications that could be costly. If you are interested in learning more about the 10-year rule, please consult with us so we can determine if this is a good strategy for you.

The Required Minimum Distribution Age Increased to 72

The SECURE ACT increased the required minimum distribution (RMD) age to 72 from 70 ½. Required Minimum Distributions were created to ensure that individuals spend their retirement savings during their lifetime and not use it for estate planning purposes to transfer wealth to beneficiaries. The change from 70 ½ to 72 reflects the increasing life expectancy of Americans. Under the SECURE Act, distributions are required to begin by April 1st of the year after you reach 72.

Many times, Qualified Charitable Distributions (QCDs) are used as a proactive tax planning strategy for anyone over 72 taking an RMD. QCDs of up to $100,000 are available to an IRA owner over 70 ½. An amount is directly given to an eligible charity processed as a QCD counts toward your RMD requirement and reduces the taxable amount of your IRA distribution. This QCD lowers both your adjusted gross income and taxable income, resulting in a lower overall tax liability. It also lowers your income for purposes of calculating if your social security is taxable.

By using, or preparing to use, a QCD, you can potentially meet your RMD requirements and satisfy your charitable intents, all while reducing your taxes. This is an area where a financial professional can offer some suggestions and strategies. We would be happy to discuss with you whether or not this tax-saving strategy could be beneficial to your specific situation.

Anyone with Earned Income Can Contribute to a Traditional IRA

The SECURE Act permanently removed the age limit at which an individual can contribute to a traditional IRA. Now, any American with earned income can continue to contribute to retirement plans regardless of age. Previously, after age 70 ½, an individual was limited to contributions to ROTH IRAs and could no longer contribute to a traditional IRA. Starting in 2020, the SECURE Act allowed anyone that is working and has earned income to contribute to a traditional IRA regardless of age.

At any age, as long as you have earned income, you can make up to a $7,000 contribution ($6,000 and if age 50 and over, a $1,000 catch-up contribution) to a Traditional IRA.

Proactive Retirement Wealth Planning

The SECURE Act brought about changes that directly affect how we look at retirement fund distributions and how beneficiaries should distribute their benefits. A solid retirement plan should always take tax efficiencies into consideration. Accumulating wealth in tax-deferred accounts such as 401(k)s, traditional IRAs, and Roth IRAs is just one part of building your retirement wealth.

Another key factor that can be more complex is knowing the best strategy for withdrawing those assets in the most tax-efficient manner. Proactively planning your distribution method from your retirement accounts to minimize your tax liability is always a wise practice that can help you retain your hard-earned money. Now is a good time to review your retirement plan, including you and your beneficiaries’ tax brackets. We can help you understand and devise a well-thought-out plan for not only your retirement but for your beneficiaries as well.

As your financial professional, we strive to provide you with proactive tax planning ideas. We understand this decision can be complex and these are not easy choices. Our goal is to understand our clients’ needs and to monitor their wealth.

We can discuss your specific situation at your next review meeting or you can call to schedule an appointment. As always, we appreciate the opportunity to assist you in addressing your financial issues.

Complimentary Financial Consultation

If you are currently not a client, we would like to offer you a complimentary, one-hour, private consultation with one of our professionals at absolutely no cost or obligation to you. To schedule your appointment, please call us at (714) 597-6510 and we would be happy to assist you!

Upcoming Events

- FAN Corporate Trustee Services Webinar | Wed, Mar 23 at 6:30pm

- Understanding Dementia & Alzheimer’s Disease Webinar | Wed, Mar 30 at 6:30pm

- Spring Retirement Classes

- Investments Webinar | Wed, May 11 at 6:30pm

- Tax Planning Webinar | Wed, May 18 at 6:30pm

- Property Inheritance Webinar | Wed, May 25 at 6:30pm

- Social Security & Medicare Webinar | Wed, June 1 at 6:30pm