Market Volatility & Risk Mitigation

- 28

- Dec

In recent months, financial markets have been quite volatile. Please view the table and commentary below to see where markets stand right now, and what FAN has done to mitigate your risk.

Market Indices

FAN Benchmarks

4. 10/31/2007-2/28/2009

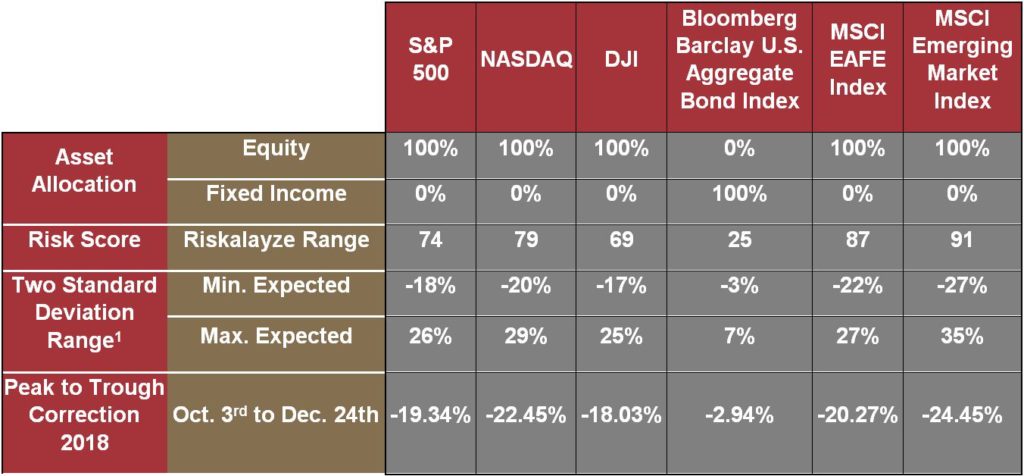

The S&P 500, NASDAQ, and Dow Jones Industrial Average indices were recently down -19.34%, -22.45%, and -18.03% respectively from peak to trough (10/03/18 to 12/24/18). These indices are each definitively in “correction” territory. It is important to recognize that portfolios with different risk objectives perform differently than these “all equity” indices.

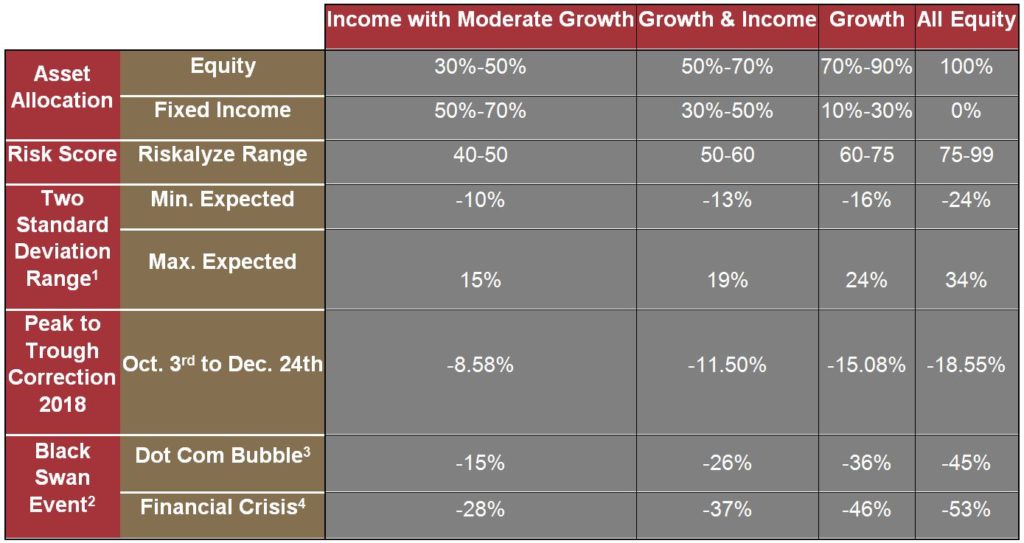

For example, you can see that the benchmark for our Growth and Income objective (Riskalyze score from 50 to 60) was down -11.50% in the same period. For a Riskalyze score in this 50 to 60 range, a decline of -11.50% is still within the normal expected volatility. At these risk scores, we can expect (with a 95% probability, or two standard deviations) downside risk to be within -13%.

In a “Black Swan Event” (three standard deviation movement) we may see returns cross the 95% probability threshold. In the two most recent “Black Swan Events” (the Dot Com Bubble from 2000 to 2002 and the Financial Crisis from 2007 to 2009), the Growth and Income Benchmark was down -26% and -37% respectively.

At this time, we are still within the “normal” two standard deviation range, and we do not expect this volatility to become a “Black Swan Event.” However, investors must always be aware of this possibility, and be prepared for it. Continue reading to see FAN’s recommendations and strategies for mitigating risk.

Risk Mitigating Strategies

We know that market volatility can be scary. To help reduce the impact of volatile markets, we recommend and implement several risk mitigation strategies to help protect your portfolio. Some of these important strategies are:

Maintaining Strong Cash Reserves – We recommend that our clients strive to maintain approximately two years of their budget need in cash (or cash-equivalent) investments. These cash reserves can be drawn from during a market decline, rather than drawing on traditional equity/fixed income investments and being forced to liquidate at a low point in the market cycle.

Additionally, with rising interest rates, some cash-equivalent investments have recently become more appealing. For example, 6-month U.S. Treasury yields are hovering around the 2.50% range (annualized) and receive the additional benefit of being exempt from state income tax.

It should be noted that this “two-year” cash reserve target can be reduced by any “near-certain” cash flows (such as Social Security or Government Pensions).

Dividend Production – You may have heard the phrase “cash is king.” What should really be said is “cash flow is king,” as reliable income streams can provide great peace of mind during times of turbulence.

In the investment world, cash flow is typically derived from two sources: Dividends and Interest. Companies that have stable income and pay out a strong dividend typically continue paying that dividend regardless of current market conditions. In many of our portfolios, we take tilts towards these income generating securities, with some portfolios having dividend yields in the 2% to 3% range. Even capital appreciation focused portfolios still maintain dividend yields in the 1.5% to 2% range.

You may be able to reduce market-related anxiety by reminding yourself that even during volatility, your portfolio is still producing cash flow.

Asset Class Diversification – Volatility is an inseparable part of financial markets. Regarding investments, we always state that only three factors can be controlled: Risk, Fees, and Taxes. Market volatility is a part of this risk component. One important way to reduce investment risk is through effective asset class diversification. We use 12 different asset classes to effectively diversify non-systematic risk. Additionally, in order to take advantage of different phases of the business cycle experienced by different global regions at any particular point in time, we also invest in international markets (both developed and emerging).

First Trust Deed Investments – While rising interest rates may make some cash-equivalents more appealing (see the treasury bill example above), they do also pose a potential risk to fixed income securities. As interest rates rise, fixed income securities typically come down in value. It is important however to maintain a fixed income allocation within a properly diversified portfolio, as they can act as a “counter-balance” to equity market volatility.

How then can we mitigate some of the investment rate risk that fixed income securities are exposed to? FAN has recently been recommending some clients explore First Trust Deed Investments as a fixed income alternative. These investments are secured by real estate and may offer higher yields than traditional fixed income securities, with reduced interest rate sensitivity. However, these investments do have their own unique risks, such as reduced liquidity, and also require more sophisticated underwriting.

Interested investors should attend one of the First Trust Deed workshops that we hold at our office, or call their paraplanner or advisor to discuss further. Please note that First Trust Deed Investments are only available to current FAN clients.

First Trust Deed Disclosure:

First Trust Deed investments have unique risks that are more fully disclosed on our firm’s current filing of form ADV which can be found on the SEC website: www.adviserinfo.sec.gov. Additional disclosures may also be found on our firm website www.financialadvisorsnetwork.com in the Resources/Disclosures & Policies section.

Graphical Disclosure:

The “Benchmark” returns by Investment Objective are calculated for the periods identified using the FAN Benchmark Portfolios as found in our firm collateral entitled “FAN Investment Menu”. The benchmark uses specific indices as a proxy for asset classes and are weighted to construct a benchmark portfolio. The purpose of a benchmark portfolio is to have a basis of comparison for returns of alternative portfolios and is not a promise or guarantee of a specified return as no one can identical construct the benchmark in an investable portfolio. However, FAN does attempt to mimic, as closely as reasonably possible and with a reasonable expense, the benchmark portfolios listed in the Investment Menu with our FAN Core Series model portfolios by investment objective.

The specified probability of returns using standard deviation is based on a Riskalyze analysis and scores using our FAN Core Series model portfolios for each respective Investment Objective. This is an idealized model that no client account allocation (and therefore, return) will exactly mimic and, therefore cannot be promised or guaranteed.