Proactive Tax Planning

- 04

- May

In the beginning, there were no income taxes or federal government. Newly organized individual colonies made ends meet by taxing a variety of things other than income, such as occupational taxes and excise taxes on specific goods. American history classrooms teach us that one of the original prompts for the United States Revolution was “taxation without representation.”

United States history reveals that early on the federal government tried to impose “direct” taxes on Americans. Later, individuals were taxed based on the value of things they owned, such as land, but not their incomes. In 1802, President Thomas Jefferson canceled direct taxes and the country went back to just collecting excise taxes.

Today’s system of federal income taxes in the United States dates back to the Civil War when Abraham Lincoln signed into law the nation’s first-ever tax on personal income to help pay for the Union war effort. It was repealed a decade later and Congress tried again in 1894 to enact a flat rate federal income tax. The U.S. Supreme Court ruled this tax was unconstitutional the following year because it did not consider the population of each state.

In 1909, Congress passed the 16th Amendment, which allowed the federal government to tax individual personal income regardless of state population. The required number of states ratified this amendment in 1913 and Americans have been required to pay federal income taxes ever since.

For 2021, the federal individual income tax has seven tax rates. These rates range from 10 percent to 37 percent. The rates apply to a filer’s taxable income, which is calculated as adjusted gross income minus either the standard deduction or allowable itemized deductions. Any income up to the standard deduction (or itemized deductions) will be taxed at a zero rate.

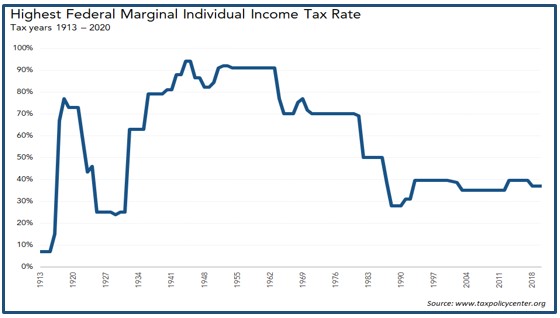

History Of Federal Income Tax Brackets And Rates

Over the 100-plus year history of the modern federal income tax, the number of brackets and rates has changed dramatically and frequently. The top marginal federal income tax rate has varied widely over time. The top rate was 91 percent in the early 1960s before the Kennedy/Johnson tax cut dropped it to 70 percent.

In 1981, the first Reagan tax cut further reduced the top rate to 50 percent and the 1986 tax reform brought it down to 28 percent. Subsequent legislation increased it to 31 percent in 1991 and to 39.6 percent in 1993. George W. Bush’s tax cuts lowered the top rate to 35 percent but it reverted to 39.6 percent when the American Taxpayer Relief Act of 2012 let the reduced top rate expire as scheduled.

The Tax Cuts and Jobs Act lowered the top rate to 37 percent starting in 2018. However, please keep in mind that the new tax rates set in that tax act are currently set to sunset or expire after 2025.

Every new presidential administration and Congress brings with them the potential for tax law change. Recent discussions from the Biden administration are showing that this is again the case. As every taxpayer has come to understand, tax rates, laws, and rules seem to be always changing.

The Federal Income Tax Rate System is Progressive

As your taxable income increases, it is taxed at higher rates. Different tax rates are imposed on income in different ranges (or brackets) depending on the taxpayer’s filing status.

In 2021, the top tax rate (37 percent) applies to taxable income over $518,400 for single filers and over $622,050 for married couples filing jointly. Additional tax schedules and rates apply to taxpayers who file as heads of household and to married individuals filing separate returns. A separate schedule of tax rates applies to capital gains and dividends.

How the Progressive Income Taxation System Works

| Tax Rate | Single | Married Filing Jointly | Married Filing Separately | Head of Household |

| 10% | Up to $9,950 | Up to $19,900 | Up to $9,950 | Up to $14,200 |

| 12% | $9,951 to $40,525 | $19,901 to $81,050 | $9,951 to $40,525 | $14, 201 to $54,200 |

| 22% | $40,526 to $86,375 | $81,051 to $172,750 | $40,526 to $86,375 | $54,201 to $86,350 |

| 24% | $86,376 to $164,925 | $172,751 to $329,850 | $86,376 to $164,925 | $86,351 to $164,900 |

| 32% | $164,926 to $209,425 | $329,851 to $418,850 | $164,926 to $209,425 | $164,901 to $209,400 |

| 35% | $209,426 to $523,600 | $418,851 to $628,300 | $209,426 to $314,150 | $209,401 to $523,600 |

| 37% | $523,601 or more | $628,301 or more | $314,151 or more | $523,601 or more |

Each tax rate applies only to income in a specific tax bracket. Therefore, if a taxpayer earns enough to reach a new bracket with a higher tax rate, their total income is not taxed at that rate, just the income that falls in that bracket. A taxpayer who has income in the top bracket has some portion of their income taxed at the lower rates of the tax schedule.

For example, a single filer with $70,000 in taxable income falls into the 22 percent bracket but does not pay tax of $16,940 (22 percent of $70,000). Instead, that taxpayer pays 10 percent of $9,950 plus 12 percent of $30,575 ($40,525 – $9,950) plus 22 percent of $19,475 ($70,000 – $40,525) for a total of $8,448.

All tax brackets for married taxpayers are larger than the size of those for singles. For filers in the highest brackets, there can sometimes be a “marriage penalty” as some couples could pay more tax filing a joint return than they would if each spouse could file as a single person.

Conversely, because most tax brackets for married couples are larger than those for singles, many married couples enjoy a “marriage bonus,” paying less in tax by filing jointly than they would if each partner filed as a single person. It is always wise to check with your tax preparer to determine the best way to file your taxes.

Why Taxes Matter

Benjamin Franklin’s old line about death and taxes resonates as true today as it did more than 200 years ago. When it comes to investing, it is not just how much you make that matters, it is how much you keep after taxes. Tax efficiency when investing is important because your pre-tax returns can be very different than your after-tax returns.

When it comes to your portfolio, your investment accounts can be divided into two main categories, taxable accounts (like a personal account) and tax-advantaged accounts (such as a retirement account). Even among retirement accounts, there are differences. For example, a ROTH IRA is free from future taxes, but a traditional or rollover IRA or 401k could be taxed when distributions are taken. When looking over your holdings, taxes DO matter.

Long-Term Capital Gains

Capital gains are the profits from the sale of an asset such as shares of stock, land, a business, and generally, are considered taxable income. How much these gains are taxed depends a lot on how long you held the asset before selling. One advantage many taxpayers try to capitalize on is the favorable rate on long-term capital gains.

The short-term capital gains tax is a tax on profits from the sale of an asset held for one year or less. The short-term capital gains tax rate is your ordinary income tax rate (your marginal tax bracket).

The long-term capital gains tax is a tax on profits from the sale of an asset held for more than a year. The long-term capital gains tax rate is 0%, 15%, or 20% depending on your taxable income and filing status. They are generally lower than short-term capital gains tax rates.

The amount you make on the sale of an item eligible for capital gains rates is your capital gain. The amount you lose is a capital loss. Investors can use investment capital losses to offset gains.

For example, if you sold a stock for a $20,000 profit this year and sold another at a $10,000 loss, you will be taxed on capital gains of $10,000. This difference between your capital gains and your capital losses is called your “net capital gain.”

Taxpayers whose capital losses exceed their gains can deduct the difference on their tax return, up to $3,000 per year ($1,500 for those married filing separately). Like income taxes, capital gains taxes are progressive.

Long-Term Capital Gains – 2021

| Tax Rate | Single | Married |

| 0% | $0 – $40,400 | $0 – $80,800 |

| 15% | $40,401 – $445,850 | $80,801 – $501,600 |

| 20% | $445,851+ | $501,601+ |

How A Proactive Tax Planning Approach Could Benefit You

Tax planning is different than tax preparation. When an investor takes a proactive tax planning approach, they are considering taxes in the equation. There are a variety of tax planning strategies that a skilled financial professional can review for clients.

These include:

- Maximizing the use of retirement plans,

- Annual tax loss and gain harvesting,

- Charitable giving,

- Asset location,

- ROTH IRA conversions,

- Waiting for long term capital gains vs. taking short-term capital gains,

- Choosing tax-efficient investments,

- Designing a tax-efficient Required Minimum Distribution (RMD) strategy,

- Family tax bracket management strategies.

A well-planned proactive tax minimization strategy includes reviewing your tax forms and situation to understand your circumstances. It then includes a conversation of discussing which strategies may or may not apply to your set of circumstances.

Proactive Tax Planning and Our Goal for Clients

We would always like our clients to maximize their wealth and best navigate their circumstances so our goal is to stay knowledgeable about Proactive Tax Planning and to try to offer our clients our best ideas. Tax rules and laws have a long history of changing. We believe a proactive approach to tax planning could yield better results than a reactive one.

For example, one of our primary objectives is to work with clients to explore efficient ways to draw down retirement savings and transfer wealth. We try to look at your financial picture from a comprehensive lens which allows us to recommend the best way to set up, manage, and distribute your wealth.

When it comes to tax efficiency, we try to focus on not just what you make, but what you keep. To discuss your situation with us, bring it up at our next meeting or call our office.

Please share this report!

This year, one of our goals is to offer our services to several other people just like you! Do you know someone who could benefit from our services? We would be honored if you shared this report with someone else.

Upcoming Webinars

Join us for one of our upcoming complimentary webinars:

- FAN Corporate Trustee Services Webinar | Wed, May 12 at 6:30pm PT

- Tax Planning Webinar | Wed, May 19 at 6:30pm PT

- First Trust Deed Info Session Webinar | Wed, May 26 at 6:30pm PT

We will also be holding a variety of other webinars over the course of the year that we would love for you to attend.